How to Prepare and Interpret a Cash Flow Statement

The cash flow statement, or statement of cash flow, is one of the three most important financial statements, along with the balance sheet and income statement. Its role is to show how the amount of cash on the balance sheet has changed from the beginning of the period to the end

The cash flow statement, or statement of cash flow, is one of the three most important financial statements, along with the balance sheet and income statement. Its role is to show how the amount of cash on the balance sheet has changed from the beginning of the period to the end. In other words, it shows the amount of cash and cash equivalents that go into and out of the business during a specified period of time.

This article will cover how to construct and interpret the cash flow statement.

The Three Cash Flow Statement Sections

The cash flow statement is divided into three categories: cash from operating activities, cash from investing activities, and cash from financing activities.

Cash flows from operating activities represent the cash inflows and outflows related to the revenues and expenses that are reported on the income statement. This is cash generated from the company’s goods or services. For example, cash received from customers or dividends and interest on investments, and cash paid for the purchase of services and goods for resale, salaries and wages, income taxes, or interest on liabilities.

Cash flows from investing activities reflects the cash inflows and outflows that relate to the acquisition and disposition of long-term assets as well as investments in other companies’ securities. This means cash received from the sale or disposal of property, plant, and equipment, or the sale or maturity of investments in securities. It also includes cash paid for purchases of property, plant, and equipment, or purchases of investments in securities.

Cash flows from financing activities illustrate the inflows and outflows of cash to finance the company from creditors and owners. Inflows are cash received from borrowing on notes, mortgages, and bonds from creditors, or issuing stock to owners. Outflows are cash paid for repayment of principal to creditors, repurchasing stock from owners, or dividends to owners.

The total increase (or decrease) in cash for the reporting period is equal to the sum of the cash flows from operating, investing and financing activities.

How to Prepare a Cash Flow Statement

In order to prepare a cash flow statement, you will need to reference two balance sheets, a complete income statement, and know some additional information.

This first step is to use the two balance sheets to calculate the change in each account by subtracting the beginning balance from the ending balance. Then, each change, whether it be positive or negative, has to be classified as associated with operating, investing, or financing activities.

Operating activities include changes in assets, liabilities, retained earnings, accounts receivable, inventories, prepaid expenses, accounts payable, and accrued expenses. Investing activities involve changes in short-term investments, and property, plant, and equipment. Financing activities encompass changes in long-term debt, common stock, additional paid-in capital, and retained earnings (for decreases resulting from dividends declared and paid).

Cash Flows from Operating Activities

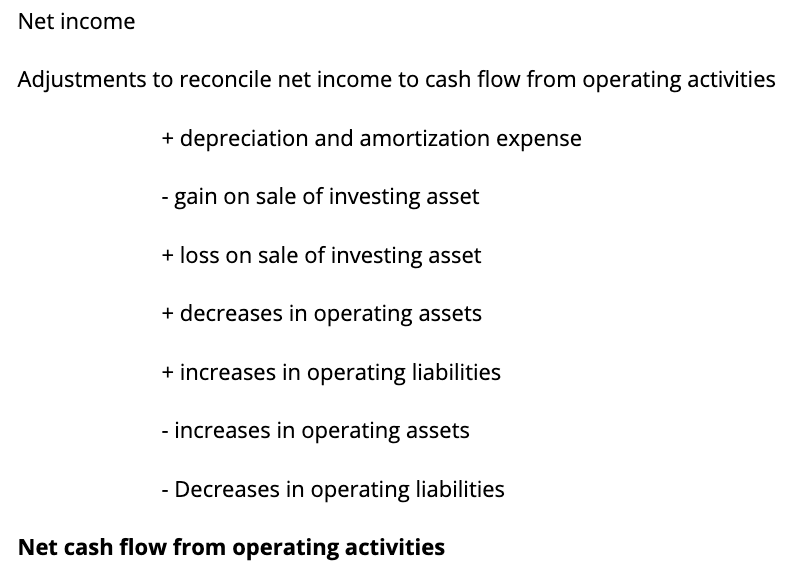

There are two methods for presenting the cash from operating activities: direct and indirect. The direct method exclusively reports cash components as inflows and outflows while the indirect method adjusts the net income to compute cash flows from operations. This means that the indirect method begins with the net income from the income statement and then removes all of the non-cash items. Although the indirect method is more common, both methods arrive at the same number. Below is an example of how to adjust net income using the indirect method.

A tip to remember how to adjust net income is to add the change in cash when there is a decrease in an operating asset or when there is an increase in an operating liability. Vice versa, subtract the change when there is an increase in an operating asset or when there is a decrease in an operating liability.

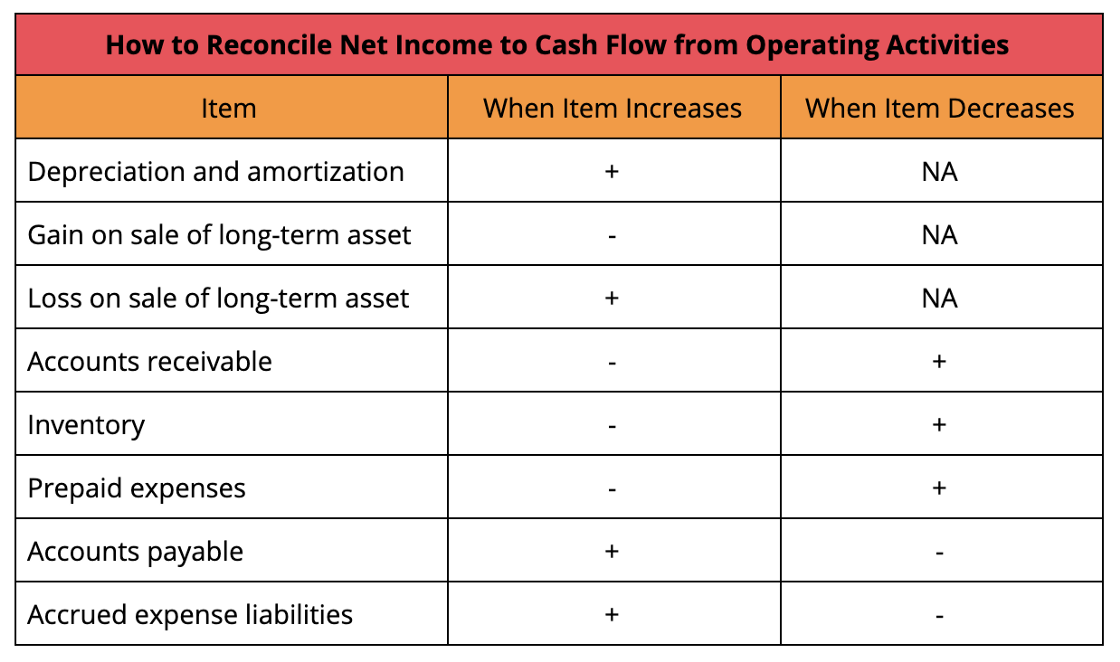

Here is a more complete table to reference when deciding whether to add or subtract a specific change in an account.

Once we have computed the cash from operating activities, we also need to know how to interpret it.

Computing the quality of income ratio (or quality of earnings ratio) is helpful to determine the company’s ability to generate cash through operations.

Quality of income ratio = cash flow from operating activities / net income

A high ratio, greater than 1, would indicate a greater ability to finance operating and other cash needs from operating cash inflows; which means high quality earnings.

Cash Flows from Investing Activities

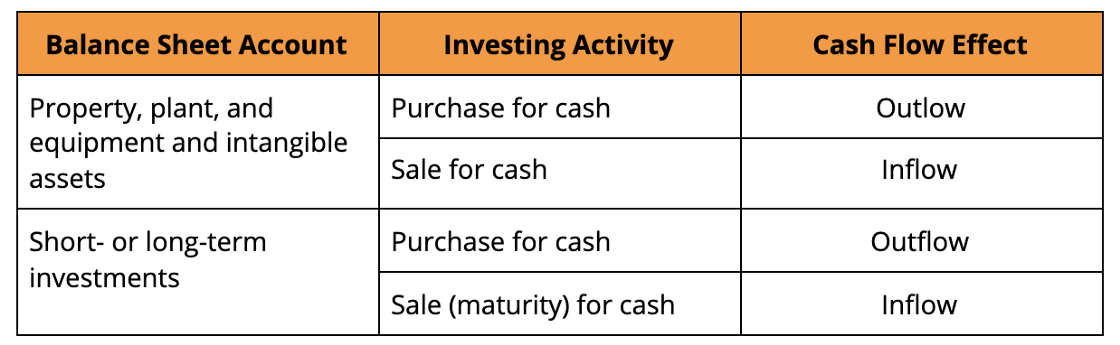

For the cash flow from investing activities section of the cash flow statement, we have to look at the property, plant, and equipment, and short or long-term investments accounts on the balance sheet. In terms of the property, plant and equipment account, purchases for cash represent an outflow while sales for cash are an inflow. Similarly, for short or long-term investments, purchases for cash are outflows while sales for cash are inflows.

It is important to include only the purchases that have been paid for with cash or cash equivalents. Also included are the proceeds from the sale of assets, no matter whether they were sold at a profit or loss.

Two calculations that can be done to determine the company’s ability to finance its growth requirements are the capital acquisition ratio and free cash flow.

Capital acquisitions ratio = cash flow from operating activities / cash paid for property, plant, and equipment

The capital acquisition ratio indicates the company’s finance capital expenditures with internal sources. Therefore, a high ratio means that the company is less likely to require outside financing.

Free cash flow = cash flow from operating activities — capital expenditures

Free cash flow is a measurement of the amount of cash a company has after it has accounted for the cash used to maintain the capital assets. A positive free cash flow is viewed as a good indication of financial agility because the company has enough cash to satisfy its obligations.

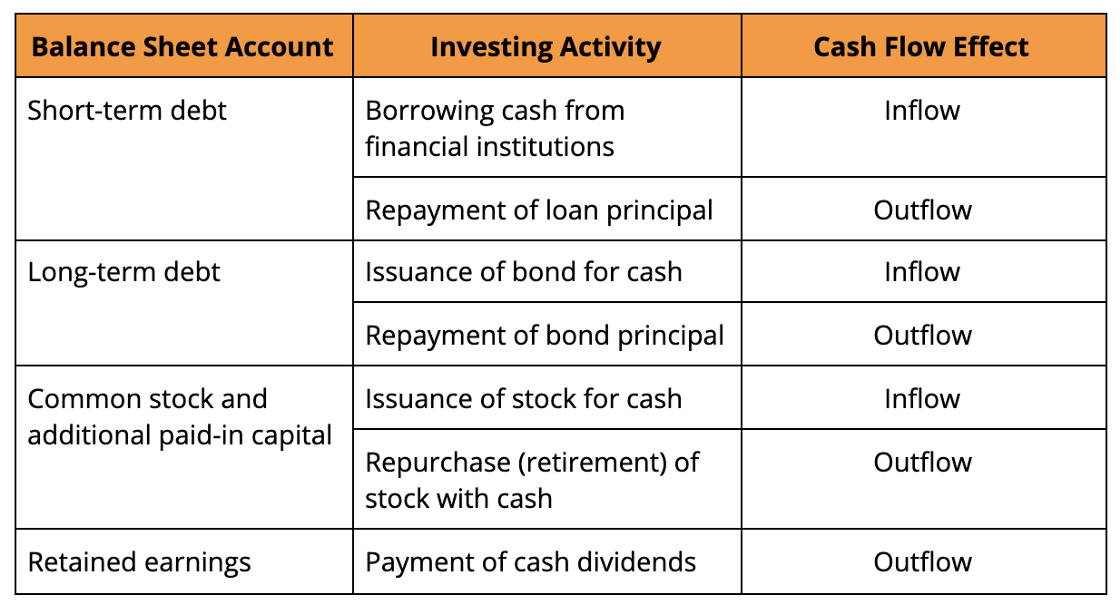

Cash Flows from Financing Activities

The cash flow from financing activities portion of the cash flow statement uses the short and long-term debt, common stock, and additional paid-in capital, and retained earnings accounts of the balance sheet.

Borrowing cash from banks or other financial institutions is classified as an inflow while the repayment of the loan principal is an outflow. Issuance of bonds and stock for cash is an inflow while repayment of bond principal or repurchase of stock with cash is an outflow. Finally, the payment of cash dividends is reported as an outflow.

All of these transactions must involve cash, otherwise, they should not be included in this section.

If the cash flow from financing activities is positive, it means that more money is coming into the company than the amount that is leaving the company. A negative cash flow from financing activities could either mean that the company is repaying debt or that it is paying dividends and repurchasing stock.

The end of period cash and cash equivalents amount reported on the balance sheet is equal to the beginning of the period amount on the balance sheet plus the net increase or decrease in cash and cash equivalents.

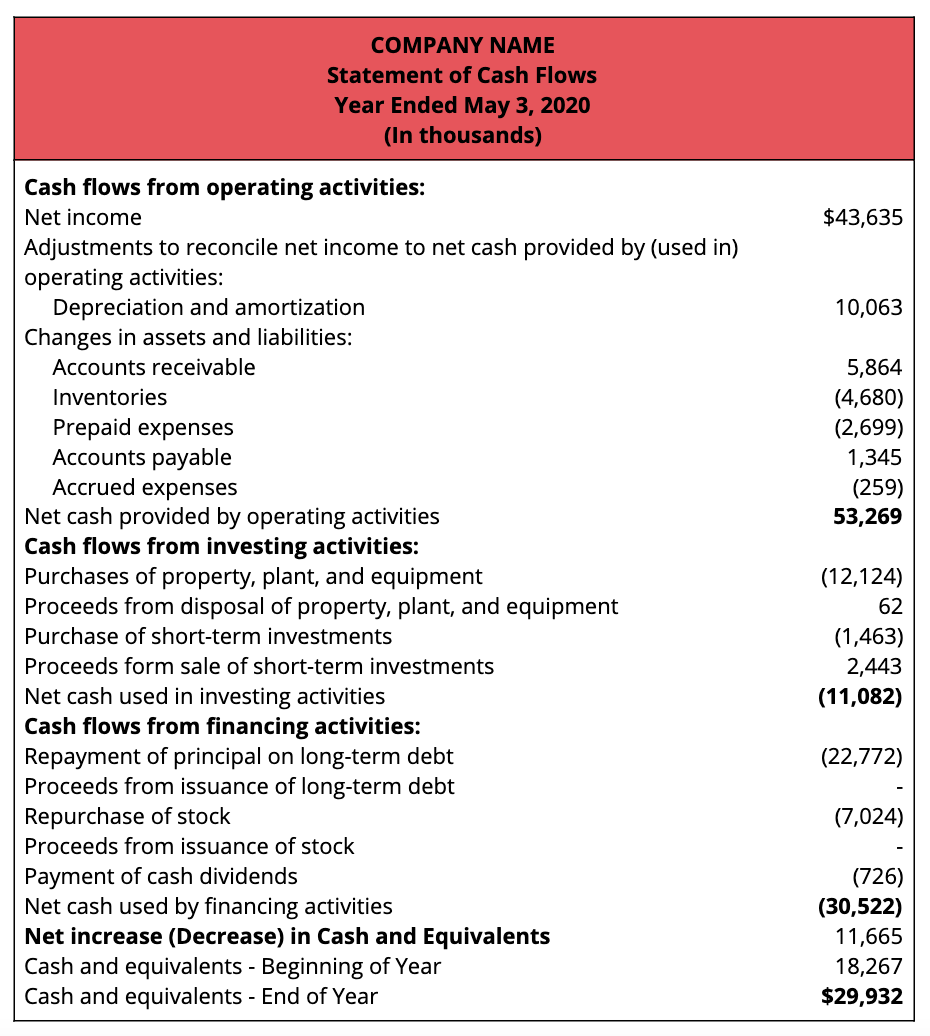

This is an example of how a complete cash flow statement looks like.

Disclosures

The biggest limitation of the cash flow statement is that it omits non-cash transactions. However, some supplemental information must be included in the footnotes of the cash flow statement. This includes the investing and financing activities that do not have an effect on the cash flow, and, for the companies that use the indirect method of presenting cash flows, the cash paid for interest and income taxes.

Why is it Important?

Along with the balance sheet and the income statement, the cash flow statement is one of the most important financial statements. But exactly why is that?

1.It tells investors where the money went

Since it reports the inflows and outflows over a period of time, the cash flow statement is often used by investors to better understand where the cash is coming from and where it goes. It holds information about a firm’s liquidity which is used by creditors to determine whether the company can cover its operating expenses.

2. It helps you make more informed financial decisions

By analyzing a cash flow statement, business owners can examine how their business growth is being financed, whether it is done by using profits or by borrowing money. This can then help evaluate what areas of the business are using up too much cash and which require more funds.

3. It is a measurement of business success

The cash flow statement tracks how much cash is generated and spent by a business during a specific period of time. As a result, it can be used for comparison between different firms and thus contributes to gaining an accurate picture of the company’s overall performance.

Regulations

The Generally Accepted Accounting Principles (GAAP) and the International Financial Reporting Standards (IFRS) categorize cash flows from operating activities differently. For this reason, it is important to pay attention to the different regulations and stick to one method of accounting.

Conclusion

The statement of cash flows shows the amount of cash and cash equivalents that go into and out of the business during a specified period of time.

Overall, having a positive cash flow is important because it means that the company is somewhat liquid, however, it does not guarantee business success.

The cash flow statement is an essential financial statement because it helps analysts evaluate a company’s ability to meet ongoing funding requirements, contribute to long-term growth, pay dividends and meet future expansion requirements.

While the cash flow statement measures changes in cash and cash equivalents, it is limited in its ability to assess non-cash transactions. It is thus important to look at all three financial statements (balance sheet, income statement, and cash flow statement) to gain a full understanding of the business’ health.